First Home Buyers: Don't Let Your HECS Debt Hold you Back — Find Out How Much You Can Actually Borrow Today

Most lenders penalise you for your student loan. We specialise in finding the ones that don't — and with $50M+ in home loans funded, we know exactly how to get HECS-burdened first home buyers in their home.

CLICK BELOW TO WATCH FIRST!

Next Step: Complete the 30-second quiz below to find out where you stand!

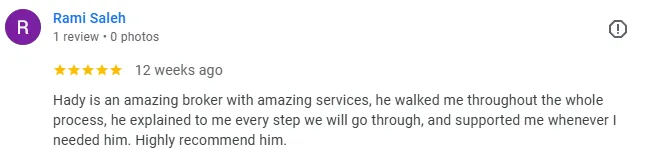

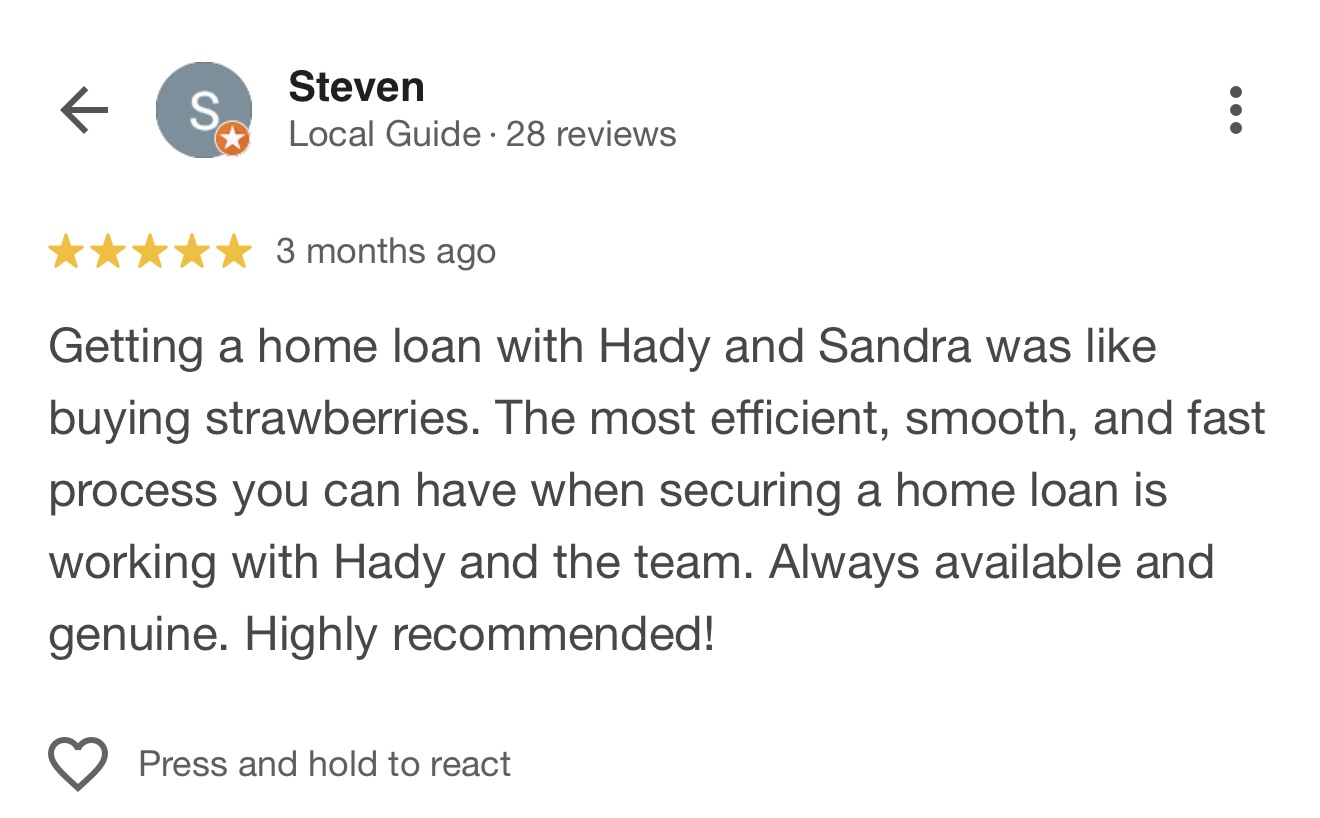

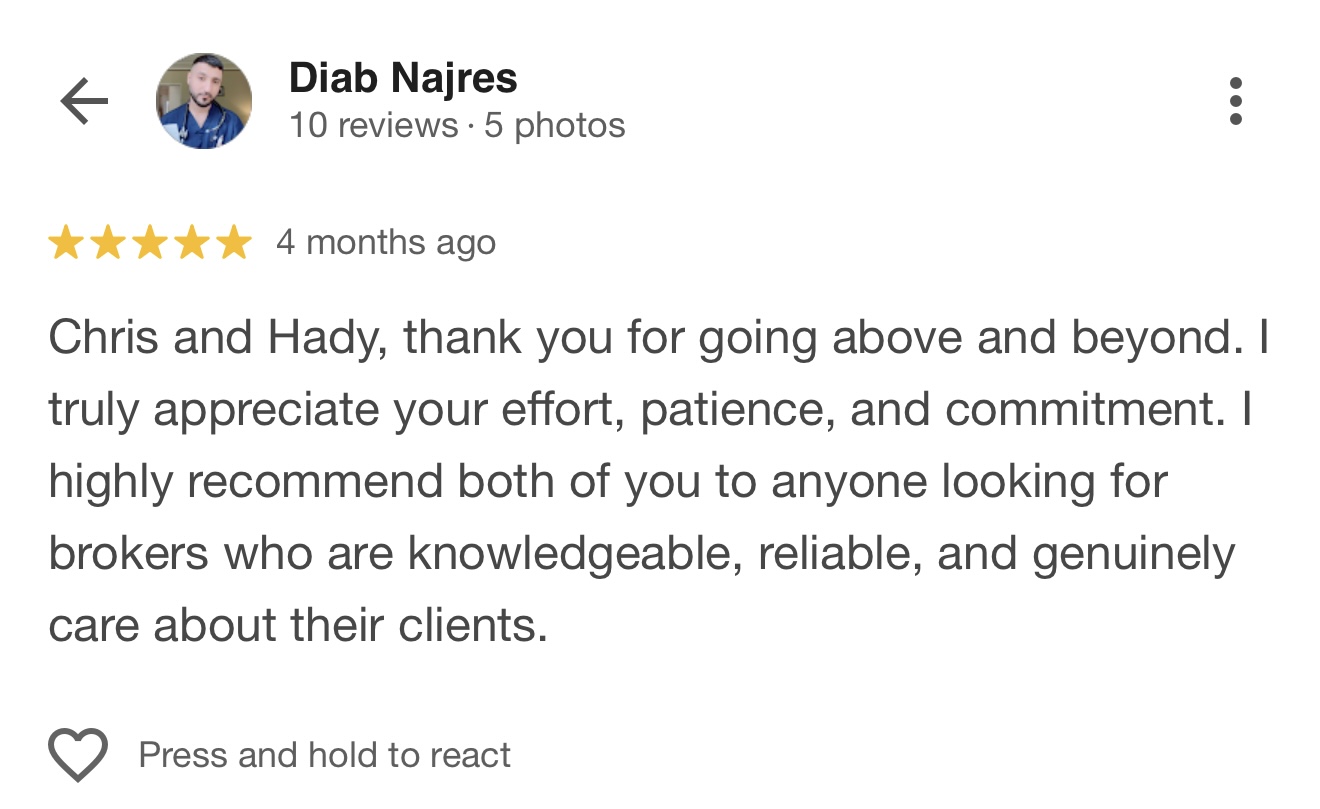

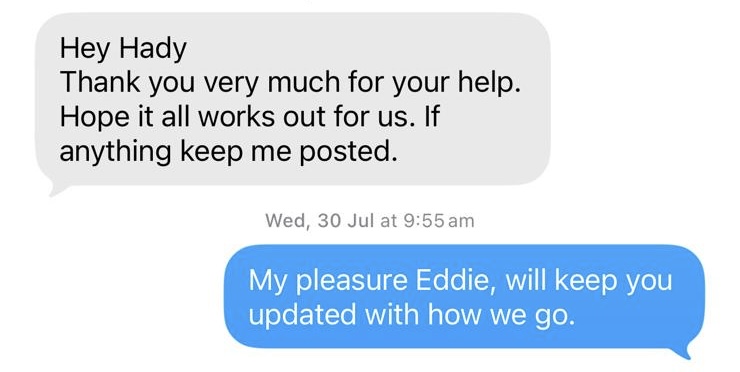

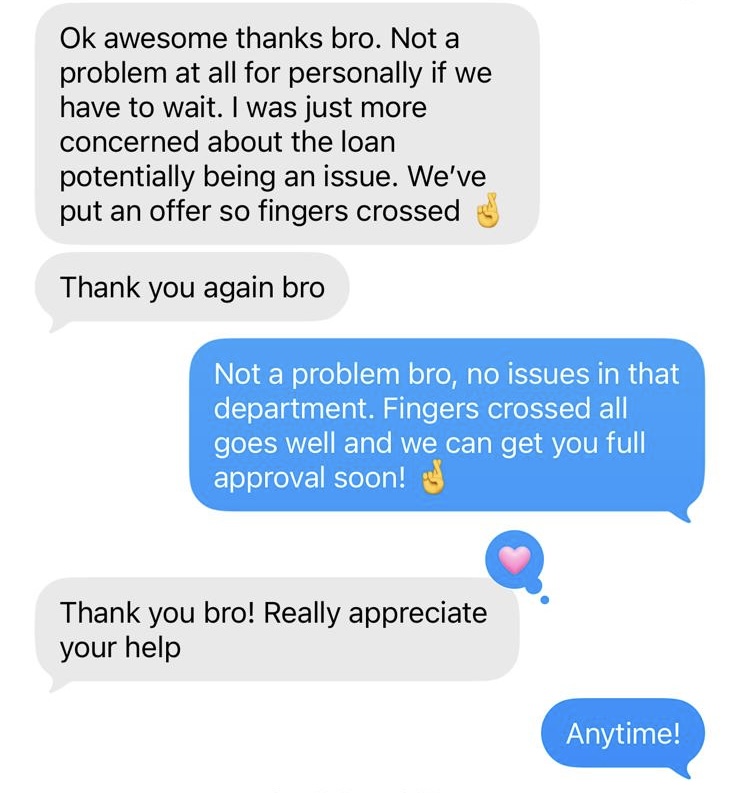

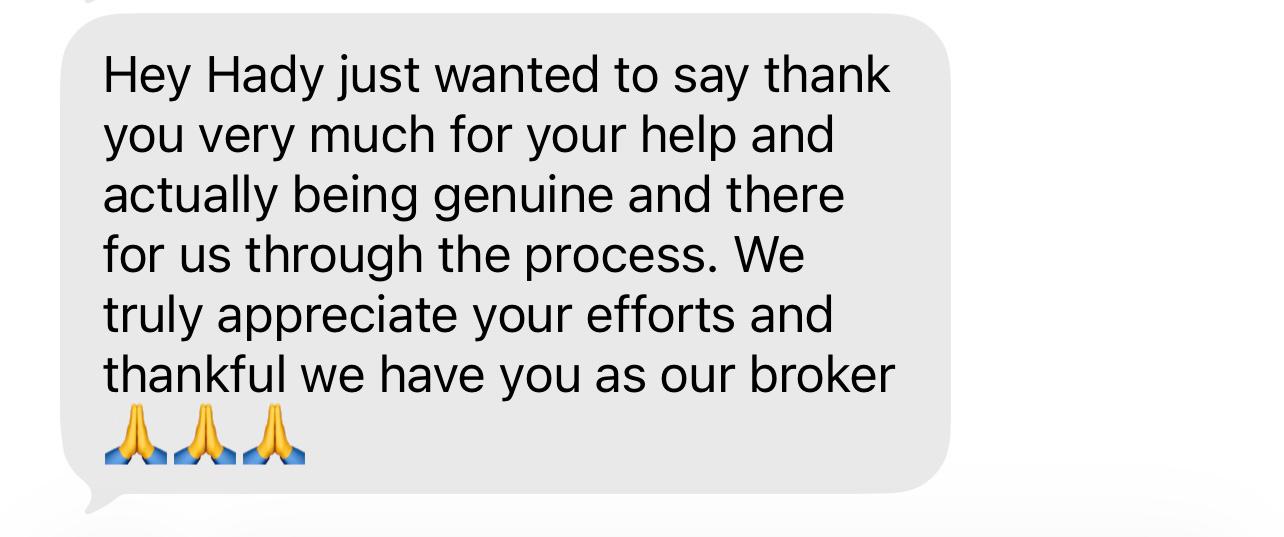

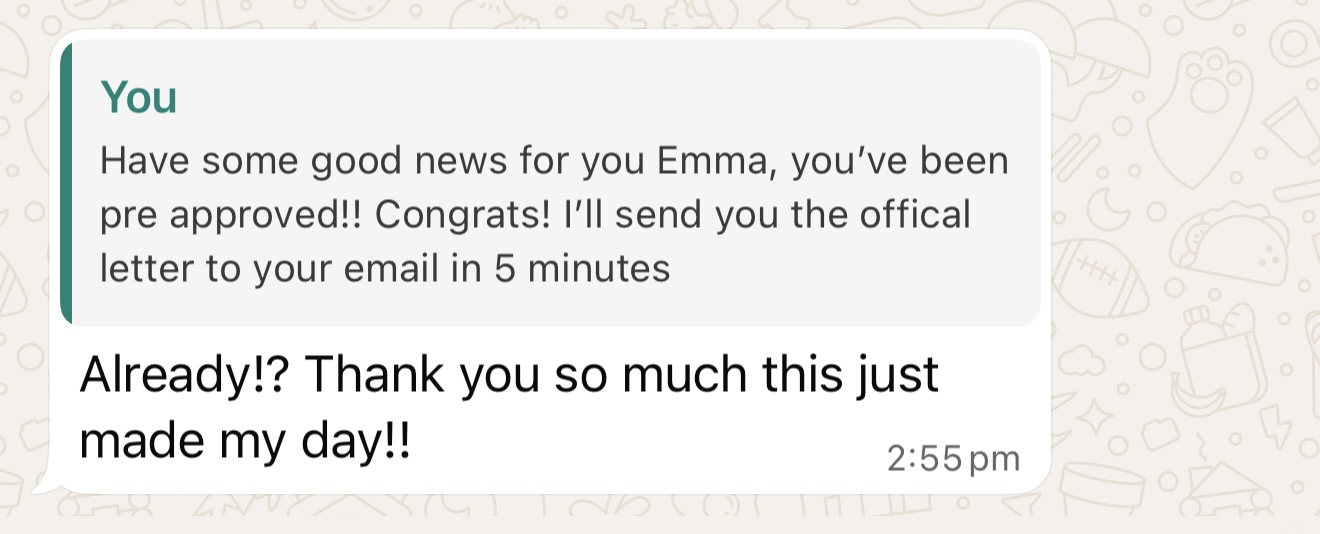

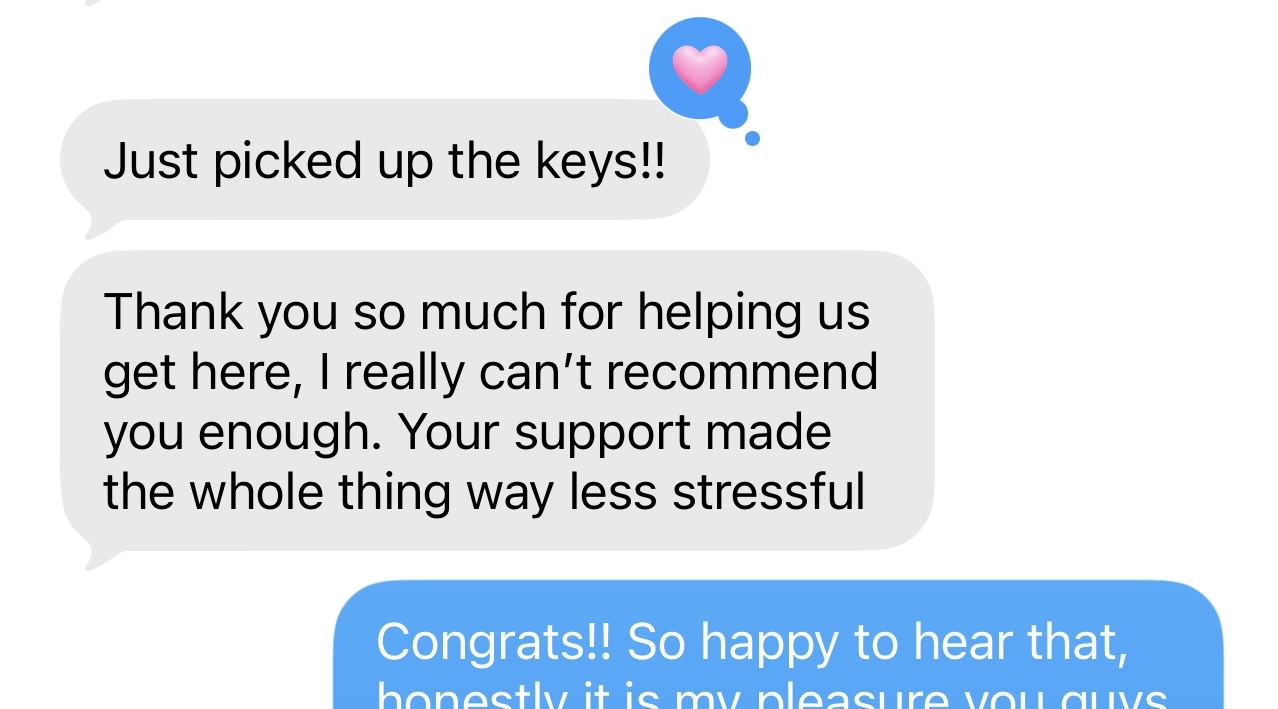

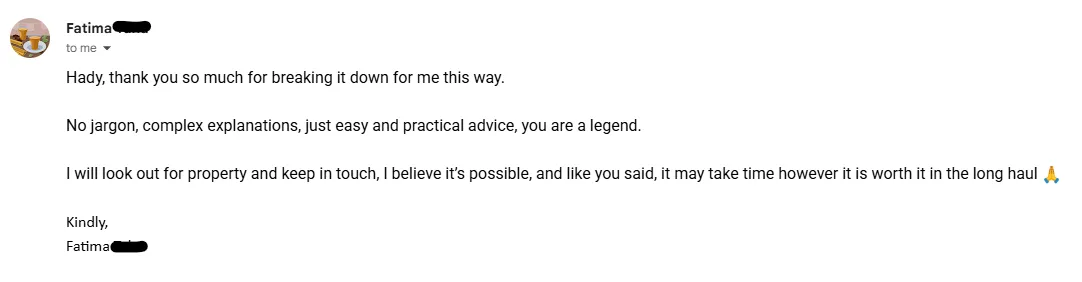

TESTIMONIALS

What others are saying

STILL NOT SURE?

Frequently Asked Questions

Here's what we usually get asked

How much deposit do I need as a first home buyer?

Most lenders require a minimum 5% deposit to purchase a property. If your deposit is under 20%, Lenders Mortgage Insurance (LMI) may apply.

At MotivMortgage, we don’t just look at the minimum — we look at the smartest pathway. We assess your eligibility for government schemes, explore options to reduce LMI, and structure your loan strategically so you can enter the market with confidence.

What is Lenders Mortgage Insurance (LMI)?

Lenders Mortgage Insurance (LMI) is a one-off premium that protects the lender when a borrower contributes less than a 20% deposit.

In many cases, LMI allows you to buy sooner rather than waiting years to save a larger deposit. We clearly outline the cost, its impact on your repayments, and whether there are ways to minimise or avoid it altogether.

How much can I borrow?

Your borrowing capacity is determined by your income, existing commitments, living expenses, and deposit size.

At MotivMortgage, we conduct a detailed serviceability assessment — not just a quick estimate. This gives you a realistic borrowing range so you can search confidently and negotiate from a position of strength.

What is pre-approval and do I need it?

Pre-approval is a conditional approval from a lender confirming how much you can borrow before you purchase.

It provides clarity around your budget, strengthens your negotiating position, and shows agents you are a serious buyer. For first home buyers, securing pre-approval is one of the most important first steps.

What government grants or schemes are available to first home buyers?

Eligible buyers may access initiatives such as the First Home Owner Grant, stamp duty concessions, and deposit guarantee schemes.

These programs can significantly reduce upfront costs, but eligibility criteria can be complex. MotivMortgage manages the entire process, ensuring all relevant applications are lodged correctly and no opportunity is overlooked.

Can I still qualify if I have HECS debt?

Yes. Many of our first home buyers have HECS debt. Different lenders treat it differently, which is why understanding lender policies is important.

What costs should I budget for besides the deposit?

Beyond your deposit, you may need to budget for stamp duty (if applicable), conveyancing fees, inspections, and lender-related charges.

We provide a complete cost breakdown upfront. Transparency is a core principle at MotivMortgage — you’ll understand the full financial picture before committing to anything.

How long does the loan approval process take?

Pre-approval is typically secured within a few business days, while full approval may take one to two weeks depending on the lender and the complexity of your application.

We proactively manage the process, liaise directly with lenders, and keep your application moving to ensure timelines are met.

Can I still get a home loan if I have existing debts?

Existing debts such as car loans, HECS, or credit cards are factored into your assessment — but they do not automatically prevent approval.

We structure your application carefully to present your financial position in the strongest possible way, while ensuring your repayments remain comfortable and sustainable.

Why use MotivMortgage instead of going directly to a bank?

A bank can only offer its own products. As an independent mortgage broker, MotivMortgage has access to a panel of lenders, allowing us to compare multiple options and tailor a solution specific to you.

Beyond comparing rates, we negotiate on your behalf, manage documentation, and guide you through every step — delivering expertise, efficiency, and strategic advantage.

What happens after my loan settles?

Settlement marks the beginning — not the end — of our relationship.

We continue to monitor your loan’s competitiveness and remain available to review your structure as your circumstances evolve. Your mortgage should adapt as your life grows.

Is there any cost for this?

Not out of your own pocket. Mortgage brokers are typically paid by the lender once your loan settles. This payment usually includes an upfront commission and a smaller ongoing commission for the life of the loan. This means there is no upfront cost to you.

What if i don't want to buy now?

No worries! Chatting with us now means you’ll have a clear plan and roadmap for the future, so when the time comes to buy your first home, you’re ready, confident, and stress-free.

Helping Everyday Australians Own Their First Home — Even when you dont know where to start.

(First home buying made simple — no confusion, no guesswork.)

Just some of the situations we help with...

Overwhelmed by advice and need real guidance for the next step

worried your deposit isnt enough and need to keep saving

Can't figure out which schemes and grants apply to you

Tired of renting and want to be building equity for yourself

Anxious about what you can actually afford to borrow

Afraid of being trapped in a 30 year mortgage

Some Lenders On Our Panel!

OWner & broker at Motivmortgage

Hey, I'm Hady

Specialist in First Home Buyer Finance

$50M+ in Home Loans Funded

Future Padel World Champion

Copyrights 2025 | MotivMortgage™ | Terms & Conditions